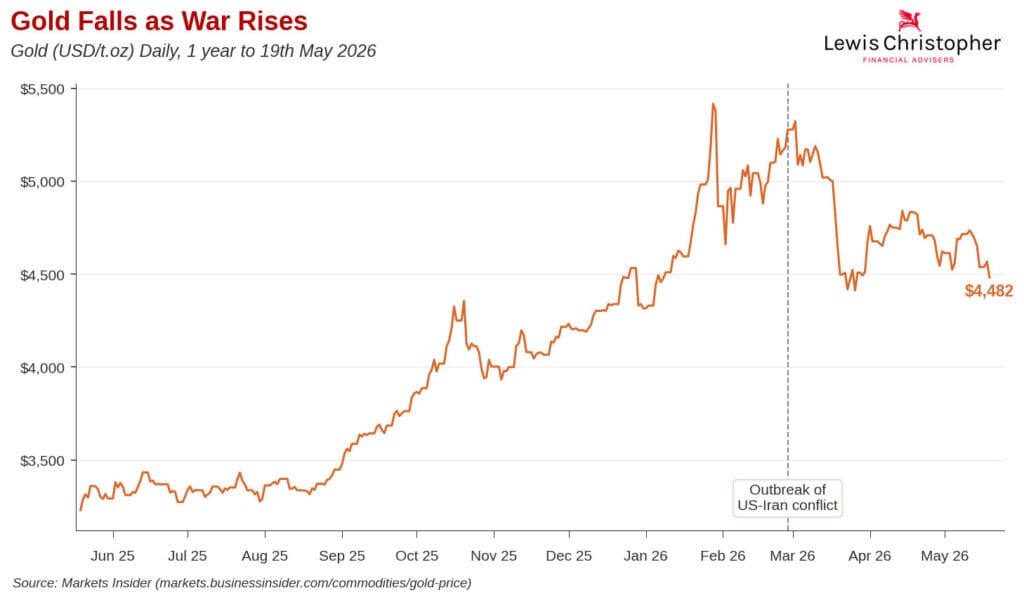

Gold has had an extraordinary, and at times counterintuitive, year so far. It opened 2026 at around $4,384/oz, the metal rallied sharply through January to set an all-time high of $5,589/oz on 28 January, driven by continued dollar weakness, persistent central bank buying, strong ETF inflows, and rising geopolitical risk ahead of the Iran nuclear standoff. That print marked the first time gold had ever traded above $5,500 — a level that would have looked extreme even twelve months earlier. Year-to-date the metal remains up around 3%, but the path has been anything but linear: gold is currently trading near $4,500/oz, roughly 20% below its January peak.

The behaviour around the outbreak of the US-Iran conflict has surprised many. Conventional wisdom says gold should rally on war as it is seen as a ‘safe’ haven — yet from 27 February (the eve of the US/Israeli strikes on Iran) to today, gold has fallen around 14%, while Brent crude has surged roughly 40%, climbing from $70 to around $100/bbl. The two assets investors traditionally pair as inflation and geopolitical hedges have moved sharply in opposite directions for the first time in recent memory.

The explanation lies in the secondary effects of the conflict rather than the conflict itself. The effective closure of the Strait of Hormuz — through which roughly 20% of global oil and gas transits — took an estimated 14.5 million barrels per day of Persian Gulf production offline and pushed oil above $100/bbl. That energy shock fed straight through to inflation, with US CPI accelerating to 3.8% in April, the highest reading since May 2023. That, in turn, killed the Fed rate-cut narrative. Markets entered the year pricing two to three cuts in 2026; expectations now price zero for the full year, with a hike judged more likely than a cut on a twelve-month view. Rising rate expectations and a rebounding dollar — both structural negatives for non-yielding gold — have done the work to press gold’s price lower, compounded by profit-taking and the unwinding of leveraged speculative positions accumulated during 2025’s bull run.

The reverse logic also explains recent rallies on ceasefire headlines: when de-escalation looks plausible, oil eases, rate-cut hopes revive, and gold trends higher. In other words, gold is currently trading less as a war hedge and more as a rate sensitivity and dollar trade.

It is also worth noting that the structural case may not have broken. In Q1 2026 total gold demand hit 1,231 tonnes worth a record $193bn, with central banks net-purchasing 244 tonnes — up 3% year-on-year — and bar and coin demand rising 42% to its second-highest quarterly total on record. Most major institutional forecasters, including J.P. Morgan, UBS and State Street, continue to see year-end 2026 prices at or above $5,000/oz, and view the current pullback as a correction within an ongoing structural bull market rather than a regime change.

This article contains general information only. This is not a financial promotion and is not intended as a recommendation to buy or sell any particular asset class, security or strategy.All information is correct as at 13/05/2026 unless otherwise stated. The expressed opinions are based on current market conditions, they may differ from those of other investment professionals and are subject to change without notice. This communication contains information on investments which does not constitute independent research.

Published by our partners at FE Invest.The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is not a reliable indicator of future performance.