Iran Conflict – What is driving markets?

Uncertainty has unsettled markets As we pass one week since…

Over the weekend the US and Israel launched a military assault on Iran with strikes on military and infrastructure targets. The Iranian head of state, Ayatollah Ali Khamenei, was killed in a strike on his compound. The attack follows an extensive build-up of American military in the Middle East as well as weeks of negotiations aimed at limiting Iran’s nuclear capabilities.

Iran has responded with missile attacks on Israel and US military targets. It has also attacked American allies including the UAE, Qatar, Kuwait and Saudi Arabia – with oil infrastructure a particular target. Attacks on shipping through the narrow Strait of Hormuz have temporarily closed the major sea route for oil and gas exports from the region.

The situation is changing very quickly as more countries are dragged into the conflict. Despite the death of Ayatollah Khamenei, Iran’s military response continued without interruption as many senior political and military leaders have vowed to continue fighting.

President Trump said the bombing campaign could continue for weeks as his administration has called for regime change in Iran. However, there is very little public support among US voters, and this may limit how long the US is willing to maintain its assault.

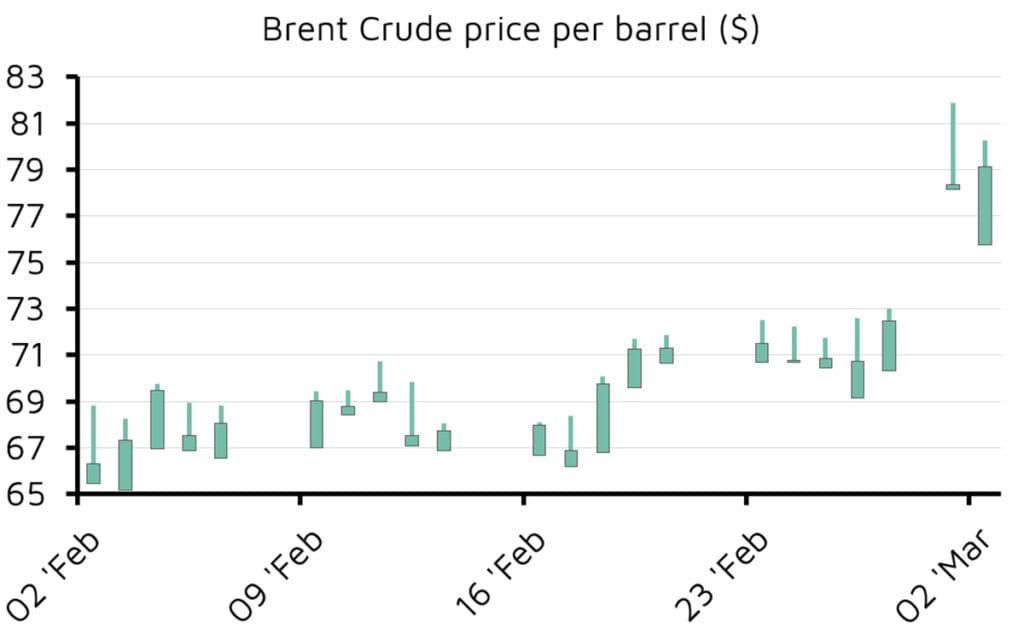

The closure of the Strait of Hormuz as well as attacks on energy infrastructure have driven up energy prices. Brent crude rose to $82 per barrel on Monday, up from $71 at Friday’s close. Heating oil jumped 14%, and European natural gas prices climbed 50%.

Equities fell as markets reopened after the weekend. Many Asian and European markets declined between 2 and 3%. However, energy, defence and shipping stocks rallied. Maersk gained more than 5% and Shell, BP and TotalEnergies rose by a similar margin.

Source: Investing.com, 02/02/2026 to 02/03/2026

Defence names were mixed: BAE Systems rose 6.6% but Rheinmetall fell 3.5%. European airlines, banks and hospitality stocks declined sharply. IAG, the owner of British Airways, fell 8.9%, and Air France-KLM dropped 7%. US markets have also started the week on the back foot.

The conflict has driven up some haven assets as gold gained 2%, and the US dollar has strengthened against most major currencies, including sterling, as investors move into US Treasuries.

Inflation in the US and UK has been slowing for the last six months after accelerating last summer and European headline inflation recent dropped below its target of 2%. However, oil and gas prices have risen sharply in the last few days and this could reverse this downward trend if fighting drags on.

For individuals, inflation is likely to show up first in petrol prices. Domestic energy bills could potentially rise unless the conflict ends swiftly. If fighting drags this also increases the potential for inflation seeping into the price of goods if energy costs for manufacturing and distribution increase. There are also wider inflationary pressures from the conflict as the cost of insuring shipping has significantly increased due to the conflict.

The implications for financial markets and the outlook for inflation will depend on the duration and scope of the conflict. The situation is evolving rapidly and we continue to monitor financial markets to assess the impact on our portfolios.

This document is for financial advisers and their retail clients and contains general information only.

Published by our partners at FE Invest.

This is not a financial promotion and is not intended as a recommendation to buy or sell any particular asset class, security or strategy.

All information is correct as at 02/03/2026 unless otherwise stated. The expressed opinions are based on current market conditions, they may differ from those of other investment professionals and are subject to change without notice.

This communication contains information on investments which does not constitute independent research.

The value of your investments can go down as well as up, so you could get back less than you invested. Past performance is not a reliable indicator of future performance.